S-1: General form for registration of securities under the Securities Act of 1933

Published on May 8, 2026

Table of Contents

(State or other Jurisdiction of Incorporation Or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

Non-accelerated filer |

☒ | Smaller reporting company | ||||

| Emerging growth company | ||||||

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 8, 2026

PRELIMINARY PROSPECTUS

SUNCRETE, INC.

52,299,704 Shares of Class A Common Stock

(Inclusive of 23,714,609 shares of Class A Common Stock Issuable Upon Conversion of Class B Common Stock, 473,800 shares of Class A Common Stock Underlying Warrants, 2,525,094 shares of Class A Common Stock Underlying Pre-Funded Warrants, 1,444,445 shares of Class A Common Stock Underlying Series A Convertible Perpetual Preferred Stock and 695,110 shares of Class A Common Stock Issuable Upon Exchange of Holdco Class B Common Shares)

473,800 Warrants to Purchase Shares of Class A Common Stock

This prospectus relates to the offer and sale, from time to time, by the selling holders identified in this prospectus (collectively, the “Selling Holders”), or their permitted transferees, of (i) up to 23,446,646 shares of our Class A common stock, par value $0.0001 (“Class A Common Stock”), held by certain Selling Holders, (ii) up to 23,714,609 shares of Class A Common Stock issuable upon the conversion of 23,714,609 shares of our Class B common stock, par value $0.0001 per share (“Class B Common Stock” and, together with the Class A Common Stock, the “Common Stock”), held by certain Selling Holders, (iii) up to 473,800 shares of Class A Common Stock underlying warrants to purchase 473,800 shares of Class A Common Stock held by certain Selling Holders (the “Warrants”), (iv) up to 2,525,094 shares of Class A Common Stock underlying pre-funded warrants to purchase 2,525,094 shares of Class A Common Stock (the “Pre-Funded Warrants”), (v) up to 1,444,445 shares of Class A Common Stock issuable upon conversion of 26,000 shares of Series A Convertible Perpetual Preferred Stock, par value $0.0001 per share (the “Series A Preferred Stock”), held by certain Selling Holders, (vi) up to 695,110 shares of Class A Common Stock issuable upon the exchange of 69,511 shares of Class B common stock, par value $0.0001 per share (the “HoldCo Class B Common Shares”), of our subsidiary, Suncrete Intermediate, Inc. (“Purchaser HoldCo”), held by certain Selling Holders (the “HoldCo Rollover Securities”), and (vii) up to 473,800 Warrants held by certain Selling Holders. This prospectus also relates to the issuance by us (with respect to 75,000 of such warrants, solely to persons other than the original purchaser thereof or its affiliates), of up to 473,800 shares of Class A Common Stock that may be issued upon exercise of 473,800 Warrants registered for resale hereby. The shares of Class A Common Stock and the Warrants that may be sold by the Selling Holders and the shares of Class A Common Stock that may be issued by us are collectively referred to in this prospectus as the “Offered Securities.” We will not receive any of the proceeds from the sale by the Selling Holders of the Offered Securities.

We will receive all of the proceeds from the exercise of the Warrants for cash, if any, registered hereunder. We believe the likelihood that the Selling Holders will exercise their Warrants, and therefore the amount of cash proceeds that we would receive, is dependent upon the trading price of our Class A Common Stock. If the trading price for our Class A Common Stock is less than $11.50 per share, we believe holders of our Warrants are unlikely to exercise their Warrants. Conversely, these holders are more likely to exercise their Warrants the higher the price of our Class A Common Stock is above $11.50 per share. The closing price of our Class A Common Stock on The Nasdaq Global Market on May 7, 2026 was $15.40 per share. The Warrants are exercisable on a cashless basis under certain circumstances specified in the Warrant Agreement (as defined herein) for the Warrants. To the extent that any Warrants are exercised on a cashless basis, the aggregate amount of cash we would receive from the exercise of the Warrants will decrease.

We will bear all costs, expenses and fees in connection with the registration of Offered Securities. The Selling Holders will bear all commissions and discounts, if any, attributable to their respective sales of Offered Securities. We are registering the Offered Securities for sale by certain of the Selling Holders pursuant to registration rights agreements with certain of the Selling Holders. See the section of this prospectus titled “Selling Holders” for more information.

The Selling Holders may offer and sell the Offered Securities owned by them covered by this prospectus from time to time. The Selling Holders may offer and sell the Offered Securities owned by them covered by this

Table of Contents

prospectus in a number of different ways and at varying prices. If any underwriters, dealers or agents are involved in the sale of any of the securities, their names and any applicable purchase price, fee, commission or discount arrangement between or among them will be set forth, or will be calculable from the information set forth, in any applicable prospectus supplement. See the sections of this prospectus titled “About this Prospectus” and “Plan of Distribution” for more information. No securities may be sold without delivery of this prospectus and any applicable prospectus supplement describing the method and terms of the offering of such securities. You should carefully read this prospectus and any applicable prospectus supplement before you invest in our securities.

The Offered Securities being offered by the Selling Holders were purchased by the Selling Holders at, or are exercisable at, various prices, certain of which are below the current trading price of our Class A Common Stock. The sale or the possibility of the sale of the Offered Securities being offered pursuant to this prospectus may negatively impact the market price of the Class A Common Stock. See the section titled “Purchase Price Paid by the Selling Holders” for more information.

The Class A Common Stock being offered for resale in this prospectus (including the shares of Class A Common Stock underlying the Class B Common Stock, the Warrants, the Pre-Funded Warrants, the Series A Preferred Stock and the Holdco Rollover Securities) represent approximately 70.1% of our total outstanding Common Stock on a fully diluted basis as of May 5, 2026. The sale of all the securities being offered in this prospectus could result in a significant decline in the public trading price of our Class A Common Stock. Despite such a decline in the public trading prices, the Selling Holders may still experience a positive rate of return on the securities they purchased due to the differences in the trading price and the purchase prices at which they purchased the securities as described herein. See “Risk Factors – Future sales, or the perception of future sales, of our Class A Common Stock by us or our stockholders in the public market could cause the market price for our Class A Common Stock to decline” and “Risk Factors – Certain existing securityholders acquired their securities in the Company at prices below the current trading price of such securities, and may experience a positive rate of return based on the current trading price. Future investors in our Company may not experience a similar rate of return.”

We are a “controlled company” within the meaning of the listing rules of The Nasdaq Stock Market, LLC (“Nasdaq”). As a controlled company, we are exempt from certain Nasdaq governance requirements that otherwise apply to the composition and function of our board of directors (the “Board”). As a result, (i) our Board does not have a majority of independent directors, (ii) the compensation of our executive officers is not determined by a majority of the independent directors or a committee of independent directors, and (iii) director nominees are not selected or recommended by a majority of the independent directors or a committee of independent directors. As of May 5, 2026, the SunTx Group (as defined herein) beneficially owned approximately 82.6% of the voting power of our outstanding Common Stock. If at any time we cease to be a controlled company, we will take all action necessary to comply with the listing rules of Nasdaq, including appointing a majority of independent directors to our Board and ensuring our compensation committee and nominating and corporate governance committee are each composed entirely of independent directors, subject to any permitted “phase-in” periods.

Our Class A Common Stock is listed on The Nasdaq Global Market under the symbol “RMIX.” On May 7, 2026, the last reported sales price of the Class A Common Stock was $15.40 per share. We are an “emerging growth company” as defined under U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings.

See “Risk Factors” beginning on page 18 to read about factors you should consider before investing in shares of our Class A Common Stock and Warrants.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2026

Table of Contents

TABLE OF CONTENTS

| 1 | ||||

| 3 | ||||

| 3 | ||||

| 4 | ||||

| 6 | ||||

| 18 | ||||

| 37 | ||||

| 38 | ||||

| UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

39 | |||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

67 | |||

| 89 | ||||

| 102 | ||||

| 107 | ||||

| 114 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

120 | |||

| 123 | ||||

| 130 | ||||

| 142 | ||||

| 145 | ||||

| 150 | ||||

| 150 | ||||

| 151 | ||||

| 151 | ||||

| F-i |

Table of Contents

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 (the “Registration Statement”) that we are hereby filing with the Securities and Exchange Commission (the “SEC”) using the “shelf” registration process. Under this shelf registration process, we and the Selling Holders may, from time to time, sell or otherwise distribute the Offered Securities as described in the section titled “Plan of Distribution” in this prospectus. We will not receive any proceeds from the sale by such Selling Holders of the Offered Securities offered by them described in this prospectus. We may receive proceeds from the exercise of Warrants registered hereunder by a person other than the original holder of the Warrants or its affiliates to the extent they are exercised for cash.

Neither we nor the Selling Holders have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the Selling Holders take responsibility for and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the Selling Holders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

We may also provide a prospectus supplement or post-effective amendment to the registration statement to add information to, or update or change information contained in, this prospectus. You should read both this prospectus and any applicable prospectus supplement or post-effective amendment to the registration statement together with the additional information to which we refer you in the sections of this prospectus titled “Where You Can Find Additional Information.”

On April 8, 2026 (the “Closing Date”), Suncrete, Inc. (the “Company”) consummated its previously announced business combination pursuant to that certain Business Combination Agreement, dated October 9, 2025 (the “Business Combination Agreement”), by and among the Company, Haymaker Acquisition Corp. 4, a Cayman Islands exempted company (“Haymaker” or “SPAC”), Haymaker Merger Sub I, Inc., a Delaware corporation and a direct wholly owned subsidiary of the Company (“Merger Sub I”), Haymaker Merger Sub II, LLC, a Delaware limited liability company and direct wholly owned subsidiary of the Company (“Merger Sub II”), and Concrete Partners Holding, LLC, a Delaware limited liability company (“CPH”), following approval thereof at an extraordinary general meeting of Haymaker’s shareholders on April 2, 2026.

Immediately prior to the closing of the Business Combination (the “Closing”), on April 8, 2026, Haymaker redeemed all of its issued and outstanding public warrants to purchase Class A Ordinary Shares of Haymaker, par value $0.0001 per share (“SPAC Class A Ordinary Shares” and such warrants, the “SPAC Public Warrants”) in exchange for (i) $2.25 in cash and (ii) 0.075 SPAC Class A Ordinary Shares per SPAC Public Warrant (the “Warrant Redemption”).

Pursuant to the terms of the Business Combination Agreement, immediately prior to the Closing, on April 8, 2026, Haymaker transferred by way of continuation out of its jurisdiction of incorporation from the Cayman Islands and domesticated into the State of Delaware in accordance with Section 388 of the Delaware General Corporation Law, as amended, and the Companies Act (As Revised) of the Cayman Islands (the “Domestication” and the time at which the Domestication became effective, the “Domestication Effective Time”).

On April 8, 2026, immediately following the Domestication, Merger Sub I merged with and into Haymaker (the “Initial Merger”), with Haymaker surviving the Initial Merger as a wholly owned subsidiary of the Company (the time at which the Initial Merger became effective, the “Initial Merger Effective Time”). Immediately following the Initial Merger, Merger Sub II merged with and into CPH (the “Acquisition Merger” and, together with the Initial Merger, the “Mergers”, and together with the Domestication, and all other transactions contemplated by the Business Combination Agreement, the “Business Combination” and the time at which the Acquisition Merger became effective, the “Acquisition Merger Effective Time”), with CPH surviving the Acquisition Merger as a wholly owned subsidiary of the Company.

1

Table of Contents

References to “Suncrete,” the “Company,” “we,” “us,” “our,” prior to the Business Combination refer to CPH, and such references following the Business Combination refer to the Company in its current corporate form as a Delaware corporation called “Suncrete, Inc.” or “RMIX.”

2

Table of Contents

MARKET AND INDUSTRY DATA

Certain industry data and market data included in this prospectus were obtained from independent third-party surveys, market research, publicly available information, reports of governmental agencies and industry publications and surveys. All of the estimates of the Company’s management presented herein are based upon review of independent third-party surveys and industry publications prepared by a number of sources and other publicly available information by the Company’s management. Third-party industry publications and forecasts state that the information contained therein has been obtained from sources generally believed to be reliable, yet not independently verified. The industry data, market data and estimates used in this prospectus involve assumptions and limitations, and you are cautioned not to give undue weight to such data and estimates. Although we have no reason to believe that the information from industry publications and surveys included in this prospectus is unreliable, we have not verified this information and cannot guarantee its accuracy or completeness. We believe that industry data, market data and related estimates provide general guidance, but are inherently imprecise. The industry in which the Company operates is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section titled “Risk Factors” and elsewhere in this prospectus.

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This document contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this registration statement may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

3

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Examples of forward-looking statements include, but are not limited to, statements with respect to the expectations, hopes, beliefs, intentions, plans, prospects, financial results or strategies regarding the Company, statements regarding the plans and use of proceeds, future financial condition of the Company and performance and expected financial impacts of the Business Combination on the Company’s business, and the Company’s expectations, intentions, strategies, assumptions or beliefs about future events, results of operations or performance that do not solely relate to historical or current facts.

These forward-looking statements generally are identified by the words “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “potential,” “should,” “will,” “would,” and similar expressions or the negative of such terms or other comparable terminology. Forward-looking statements are based on assumptions as of the time they are made and are subject to risks, uncertainties and other factors that are difficult to predict with regard to timing, extent, likelihood and degree of occurrence, which could cause actual results to differ materially from anticipated results expressed or implied by such forward-looking statements. Such risks, uncertainties and assumptions, include, but are not limited to:

| • | the failure to realize the anticipated benefits of the Business Combination and any transactions contemplated thereby; |

| • | the failure of the Company to maintain the listing of its securities on Nasdaq; |

| • | costs related to the Business Combination and as a result of the Company becoming a public company; |

| • | changes in business, market, financial, political and regulatory conditions; |

| • | the ability of the Company to grow and manage growth profitably; |

| • | risks relating to the Company’s anticipated operations and business, including the success of any future acquisitions; |

| • | the Company’s ability to retain its management and key employees; |

| • | the risk that issuances of equity or debt securities, including issuances of equity securities in connection with the Company’s acquisition strategy, may adversely affect the value of the Company’s common stock and dilute its stockholders; |

| • | the risk that the Company experiences difficulties managing its growth and expanding operations following the consummation of the Business Combination; |

| • | challenges in implementing the Company’s business plan, due to lack of an operating history, operational challenges, significant competition and regulation; and |

| • | the other risks and uncertainties discussed in “Risk Factors” and elsewhere in this prospectus. |

In addition, there may be events that the Company’s management is not able to predict accurately or over which the Company has no control.

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this prospectus, which are incorporated by reference herein. If one or more events related to these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may differ materially from what we anticipate. Many of the important factors that will determine these results are beyond our ability to control or predict. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update

4

Table of Contents

or review any forward-looking statement, whether as a result of new information, future developments or otherwise. New factors emerge from time to time, and it is not possible for us to predict which will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

5

Table of Contents

PROSPECTUS SUMMARY

Overview

Suncrete is a ready-mix concrete logistics and distribution platform operating across Oklahoma, Arkansas, Texas and Louisiana with plans to continue expanding throughout the high-growth U.S. Sunbelt region through acquisitions and organic growth. We leverage operational scale, technological integration and quality control to serve a diverse base of infrastructure, commercial and residential customers. In each of our core metropolitan markets, we target to maintain leading market share positions, supported by a business model centered on dense local market coverage, optimized logistics and disciplined pricing. We believe these attributes drive attractive unit economics, high cash conversion and resilient performance across macroeconomic cycles. Our leadership team, comprised of industry veterans with extensive experience building, acquiring and improving ready-mix concrete businesses, positions us to continue expanding profitably in an industry with compelling structural growth tailwinds.

Ready-mix concrete is a crucial building material that is used in the vast majority of infrastructure, commercial and residential construction projects. We serve substantially all end markets of the construction industry in our select geographic markets. Our customer base is comprised of contractors for commercial and industrial, residential, street and highway and other public works construction. Because ready-mix concrete is highly perishable, expiring approximately 90 minutes from its creation, our trade areas are limited to the approximate 20-mile radius surrounding each of our ready-mix concrete plants. This creates an attractive market dynamic where the relevant competition is typically limited to local market players. Additionally, the Sunbelt market in which we operate and look to expand is highly fragmented, consisting of thousands of plants and hundreds of unique owners, which creates attractive competitive dynamics and opportunities for acquisitive growth in addition to organic growth.

We currently operate across Oklahoma, Arkansas, Texas and Louisiana, and we are seeking to continue expanding throughout the Sunbelt region of the United States. The Sunbelt is a high-growth region of the U.S., with attractive economic characteristics driven by significant population migration, robust infrastructure spend and commercial relocations. According to the Bureau of Economic Analysis, the Sunbelt delivers approximately 40% higher GDP growth than non-Sunbelt states. According to Federal Reserve Economic Data, the Sunbelt population growth rate is approximately 270% higher than the population growth in other regions of the United States. In addition to GDP and population growth, the Sunbelt has experienced historical tailwinds from infrastructure spend, with $140.8 billion in total federal funding allocations from the Federal-Aid Highway Apportioned Programs and Bridge Replacement and Repairs within the Infrastructure Investment and Jobs Act of 2021 (“IIJA”). The Sunbelt is also experiencing growth from significant corporate headquarter relocations, with seven of the top eight metro destinations for headquarter relocations from 2022 – 2024 being in Sunbelt states.

Core Business. Our best-in-class logistics and ability to optimize deliveries are key contributors to our route density and profitability. Our operational expertise is reinforced by our experienced staff of professional engineers and seasoned operators, whose technical insight and field execution enable us to design, operate, and continuously refine highly efficient delivery systems. This know-how is the foundation of our operating strategy and is supplemented by best-in-class technology, rigorous analytics, and the application of both proven and cutting-edge engineering techniques that enable us to deliver the right product on time and on spec. Paired with strong geographic and industry tailwinds, we believe we are well positioned for continued strong organic growth in the attractive Sunbelt region.

As of December 31, 2025, we operated 50 standard ready-mix concrete plants at 39 locations with 336 mixer trucks and 77 haul trucks. During the year ended December 31, 2025, our plants and facilities produced ready-mix concrete resulting in revenue of approximately $194.9 million. Our ready-mix concrete product revenue by type of construction activity for the year ended December 31, 2025 was approximately 47.2% commercial, 36.7%infrastructure and 15.8% residential.

6

Table of Contents

Acquisitions. Acquisitive growth is a key component of our core business strategy and complements the expansive organic growth trends that are the foundation of our business. Focused on the growing Sunbelt region, we intend to leverage our relationships in the industry to continue our path of completing accretive acquisitions in the ready-mix concrete industry. Capitalizing on the scale, operational efficiency and management best practices of our core business, we intend to apply our proprietary strategy to integrate acquisitions into our corporate functions and lift the margins of the businesses we acquire. We believe acquisitions provide opportunities to establish leadership in mature markets with fewer players where we can increase local density and deliver higher value to customers and employees within these markets.

We (and/or our predecessors) have acquired nine companies since 2016. We are in active discussions with additional potential acquisition candidates, and beyond these active conversations, we have a robust pipeline of identified potential targets throughout the Sunbelt. For information regarding recent acquisitions, see “Recent Developments” below.

Our Business

Our ready-mix concrete business engages principally in the precise formulation, efficient production and on-time delivery of ready-mix concrete to our customers’ job sites. Ready-mix concrete is a highly versatile construction material that results from combining coarse and fine aggregates such as crushed stone, sand, and cement with water and various chemical admixtures. We also provide services intended to reduce our customers’ overall construction costs by lowering the installed, or “in-place,” cost of concrete. These services include the formulation of mixtures for specific design uses, on-site and lab-based product quality control and customized delivery programs to meet our customers’ needs. We generally do not provide paving or other finishing services, which construction contractors or subcontractors typically perform. As a result, we are fundamentally a concrete logistics and distribution platform. We are not a construction services company, nor do we operate in the highly capital intensive cement business. This focus drives profitability and cash flow conversion because our business model is not capital intensive.

Our standard ready-mix concrete products consist of proportioned mixes that we produce and deliver in an unhardened plastic state for placement and shaping into designed forms at the job site. Selecting the optimum mix for a job involves determining not only the ingredients that will produce the desired permeability, strength, appearance, and other properties of the concrete after it has hardened and cured, but also the ingredients necessary to achieve a workable consistency tailored for the weather and other conditions at the job site. We are able to efficiently and accurately produce and deliver over a thousand customized mix designs, a strength which we believe is a further differentiator to our competitors.

We maintain leading local market positions by focusing on infrastructure and commercial projects which generally result in higher margins than residential projects, while still maintaining enough residential presence to diversify end market exposure and strengthen our response to shifting market demands. We believe our focus on select geographic markets with favorable industry dynamics, disciplined pricing, accretive acquisitions and prudent balance sheet leverage distinguishes us from our competition and results in superior growth and margin performance.

Recent Developments

Thunder Acquisition

On October 17, 2025, Eagle Redi-Mix Concrete, LLC, an indirect wholly owned subsidiary of the Company (“Eagle Redi-Mix”), entered into an equity and asset purchase and contribution agreement (as amended on March 27, 2026, the “Equity and Asset Purchase and Contribution Agreement”) with SRM, Inc., an Oklahoma corporation (“Schwarz Ready Mix”), SRM Leasing, LLC, an Oklahoma limited liability company (“Schwarz Leasing”), Schwarz Sand, LLC an Oklahoma limited liability company (“Schwarz Sand,” and together with

7

Table of Contents

Schwarz Ready Mix and Schwarz Leasing, the “Schwarz Entities”) and the other selling parties named therein and Schwarz Ready Mix, in its capacity as a representative of the selling parties. Pursuant to the Equity and Asset Purchase and Contribution Agreement, Eagle acquired substantially all of the assets of Schwarz Ready Mix and Schwarz Leasing and all of the issued and outstanding equity interests of Schwarz Sand (collectively, the “Thunder Acquisition”). The aggregate purchase price included $97.0 million in cash consideration ($74.3 million paid at closing and $22.7 million deferred until June 30, 2026) and 20,000,000 Company Preferred Units issued to the sellers as rollover equity.

Hope Acquisition

On April 28, 2026, two subsidiaries of the Company, Concrete Partners, LLC, a Delaware limited liability company, and Purchaser Holdco, a newly formed subsidiary of the Company, entered into a Membership Interest Purchase Agreement (the “Hope Purchase Agreement”) and related agreements with the owners (the “Sellers”) of Hope Concrete, LLC, a Texas limited liability company (“Hope”), to acquire 100% of the ownership interests of Hope and its subsidiaries, Lafayette Concrete Division LLC, a Louisiana limited liability company, and Baton Rouge Concrete Division LLC, a Louisiana limited liability company (collectively with Hope, the “Hope Companies”). The Hope Companies are in the business of concrete manufacturing, concrete production, concrete sales, and trucking of concrete, sand, rock, cement, and fly ash. On April 28, 2026, the Company completed the acquisition of the Hope Companies (the “Hope Acquisition”).

After giving effect to the transactions contemplated by the Hope Purchase Agreement, the aggregate consideration consisted of (i) 220,007 shares of Class A Common Stock issued to one of the Sellers, (ii) 69,511 shares of Holdco Rollover Securities issued to one of the Sellers and (iii) a net closing cash payment of $39,377,232.21, subject to certain adjustments as set forth in the Hope Purchase Agreement, with respect to the purchased units sold by the other Sellers. In addition, the Company paid $27.4 million to satisfy the debt obligations of Hope Concrete.

The Holdco Rollover Securities issued by Purchaser Holdco are nonvoting, have no dividend or liquidation rights and are exchangeable for an aggregate of 695,110 shares of Class A Common Stock on the terms and subject to the conditions set forth in an Exchange Agreement, dated April 28, 2026, by and among the Company, Purchaser Holdco and Foley Bros., LLC, a Texas limited liability company (the “Hope Exchange Agreement”).

Southern Louisiana Acquisition

On April 29, 2026, the Company acquired a ready-mix concrete company in Southern Louisiana for aggregate consideration consisting of (i) $31.0 million in cash at closing, (ii) 259,291 shares of Class A Common Stock issued to the sellers at closing and (iii) an earnout payment of up to $10.0 million based upon the acquired company’s achievement of specified performance criteria over a five-year post-closing performance period. The earnout is payable, if at all, in cash or Class A Common Stock, at the Company’s election, with the number of shares of Class A Common Stock issuable based upon the average closing price per share of the Class A Common Stock on The Nasdaq Global Market for the 30 consecutive trading days preceding the end of the earnout period; provided that in no event will the Company issue shares of Class A Common Stock if the issuance would exceed (a) the aggregate number of shares of Class A Common Stock that the Company may issue in compliance with the rules and regulations of Nasdaq or (b) 9.99% of the issued and outstanding shares of Class A Common Stock.

Nelson Bros. Acquisition

On May 6, 2026, the Company, through Hope, entered into a Membership Interest Purchase Agreement (the “Nelson Purchase Agreement”) and related agreements with the owners of Nelson Bros. Ready Mix, LLC, a Texas limited liability company (“Nelson Bros.”), to acquire 100% of the ownership interests of Nelson Bros.

8

Table of Contents

and its subsidiary, R & R Trucking LLC, a Texas limited liability company (collectively with the Nelson Bros., the “Nelson Acquired Companies”). The Nelson Acquired Companies are in the business of concrete manufacturing, concrete production, concrete sales, and trucking for their concrete operations (including trucking of concrete, sand, rock, cement, and fly ash for use in concrete manufacturing and production). On May 6, 2026, the Company completed the acquisition of the Nelson Acquired Companies pursuant to the Nelson Purchase Agreement (the “Nelson Acquisition”). The owners of the Nelson Acquired Companies who are also parties to the Nelson Purchase Agreement, were Randell R. Owens, Ronda A. Owens, JAO, LLC, a Texas limited liability company (“JAO”), and Owens Regional Investments, LLC, a Texas limited liability company (“Owens Regional,” and collectively, with Mr. Owens, Ms. Owens and JAO, the “Nelson Sellers”), and Jacob Owens in his capacity as representative of the Nelson Sellers.

The aggregate consideration for the Nelson Acquisition consisted of (i) 1,296,456 shares of Class A Common Stock issued to the Nelson Sellers (the “Nelson Stock Consideration”) and (ii) $42.3 million net cash payment at closing. In addition, the Nelson Sellers will be eligible to receive a contingent earnout payment of up to $18.0 million based on the achievement of a specified trailing twelve-month materials spread target by the Nelson Acquired Companies, measured as of the end of any full calendar quarter ending during the five-year period following the closing of the Nelson Acquisition, with Hope having the option to satisfy up to 50% of any such earnout payment by issuing shares of the Company’s Class A Common Stock in lieu of cash (the “Nelson Earnout Stock Consideration”), with the number of shares of Class A Common Stock issuable based upon the average closing price per share of the Class A Common Stock on The Nasdaq Global Market for the 30 consecutive trading days preceding the end of the earnout period; provided that in no event will the Company issue shares of Class A Common Stock if the issuance would exceed (a) the aggregate number of shares of Class A Common Stock that the Company may issue in compliance with the rules and regulations of Nasdaq or (b) 9.99% of the issued and outstanding shares of Class A Common Stock.

Business Combination with Haymaker

On April 8, 2026 (the “Closing Date”), the Company consummated the Business Combination pursuant to the Business Combination Agreement. Immediately prior to the Closing, on April 8, 2026, Haymaker redeemed all of its issued and outstanding public warrants to purchase SPAC Class A Ordinary Shares and the SPAC Public Warrants in exchange for (i) $2.25 in cash and (ii) 0.075 SPAC Class A Ordinary Shares per SPAC Public Warrant.

Immediately prior to the Closing, on the Closing Date, Haymaker transferred by way of continuation out of its jurisdiction of incorporation from the Cayman Islands and domesticated into the State of Delaware. At the Domestication Effective Time (a) each SPAC Class A Ordinary Share that was issued and outstanding immediately prior to the Domestication Effective Time converted automatically, on a one-for-one basis, into one share of Class A Common Stock of the post-Domestication SPAC, par value $0.0001 per share (“SPAC Class A Common Stock”), (b) each Class B Ordinary Share of Haymaker, par value $0.0001 per share, that was issued and outstanding immediately prior to the Domestication Effective Time converted automatically, on a one-for-one basis, into one share of Class B Common Stock of the post-Domestication SPAC, par value $0.0001 per share (“SPAC Class B Common Stock”), and (c) each then-issued and outstanding private warrant to purchase SPAC Class A Ordinary Shares prior to the Domestication converted automatically, on a one-for-one basis, into one private warrant to purchase SPAC Class A Common Stock (a “SPAC Private Warrant”).

On the Closing Date, immediately following the Domestication, Merger Sub I merged with and into Haymaker, with Haymaker surviving the Initial Merger as a wholly owned subsidiary of the Company. At the Initial Merger Effective Time, among other things, (a) Haymaker Sponsor IV, LLC (“Sponsor”) distributed 2,800,000 shares of SPAC Class A Common Stock (the “Dothan Founder Shares”) and 398,800 SPAC Private Warrants to Dothan Independent GP, LP (“Dothan Independent”), (b) each share of SPAC Class A Common

9

Table of Contents

Stock issued and outstanding immediately prior to the Initial Merger Effective Time was canceled and converted into one share of Class A Common Stock, (c) each share of SPAC Class B Common Stock issued and outstanding immediately prior to the Initial Merger Effective Time was canceled and converted into one share of Class B Common Stock and (d) each then-outstanding SPAC Private Warrant was automatically assumed and converted into a private warrant to purchase one share of Class A Common Stock.

On the Closing Date, immediately following the Initial Merger, Merger Sub II merged with and into CPH, with CPH surviving the Acquisition Merger as a wholly owned subsidiary of the Company. At the Acquisition Merger Effective Time, among other things, (a) each share of Class B Common Stock issued and outstanding immediately prior to the Acquisition Merger Effective Time (other than the Dothan Founder Shares) was converted into and exchanged, on a one-for-one basis, into one share of Class A Common Stock, (b) the Company issued 14,117,894 shares of Class A Common Stock to members of CPH, (c) the Company issued 3,481,776 shares of restricted Class A Common Stock upon the cancelation and conversion of certain incentive units previously granted to management of CPH, (d) the Company issued 18,414,609 shares of Class B Common Stock to members of CPH, and (e) the Company issued 2,500,000 shares of Class B Common Stock to Dothan Independent.

In addition, as previously disclosed, the Company previously entered into subscription agreements (the “PIPE Subscription Agreements”) with certain institutional investors (collectively, the “PIPE Investors”), pursuant to which (a) immediately prior to the Acquisition Merger Effective Time, the Company issued and sold to certain of the PIPE Investors in a private placement an aggregate of 8,691,573 shares of Class A Common Stock and Pre-Funded Warrants to purchase 2,525,094 shares of Class A Common Stock and (b) at the Acquisition Merger Effective Time, the Company issued and sold to certain of the PIPE Investors in a private placement an aggregate of 6,162,009 shares of Class A Common Stock, for an aggregate total subscription amount of $167.1 million (collectively, the “PIPE Investment”).

Further, on the Closing Date, immediately prior to the closing of the Acquisition Merger, the Company issued 26,000 shares of Series A Preferred Stock to the holders of CPH’s Senior Preferred Units (the “Exchanging Holders”) pursuant to that certain Securities Exchange Agreement, dated March 26, 2026, by and among the Company and the Exchanging Holders (the “Exchange Agreement”).

In connection with the closing of the Business Combination, holders of 12,628,150 SPAC Class A Ordinary Shares sold in Haymaker’s initial public offering properly exercised their right to have their shares redeemed for a pro rata portion of the trust account holding the proceeds from Haymaker’s initial public offering, and on April 8, 2026, prior to the Domestication, Haymaker redeemed 12,628,150 SPAC Class A Ordinary Shares for $11.57 per share (the “Public Share Redemptions”). As a result, on April 8, 2026, after giving effect to the Public Share Redemptions and payments to holders under prepaid forward agreements described below and before paying expenses, there was approximately $59 million remaining in the trust account.

Warrant Amendment and Redemption

On the Closing Date, prior to the Warrant Redemption, Haymaker, the Company and Continental Stock Transfer & Trust Company, in its capacity as warrant agent (the “Warrant Agent”), entered into Amendment No. 1 to the Warrant Agreement (the “Warrant Amendment”) to amend that certain Warrant Agreement, dated as of July 25, 2023, by and between Haymaker and the Warrant Agent (the “Warrant Agreement”) to effect the Warrant Redemption.

10

Table of Contents

Amended and Restated Registration Rights Agreement

In connection with the Closing, the Company, Haymaker, and Sponsor entered into an Amended and Restated Registration Rights Agreement (the “A&R Registration Rights Agreement”) amending and restating the existing Registration Rights Agreement, dated as of July 25, 2023, by and between Haymaker and Sponsor and certain other equityholders of Haymaker (the “Existing Registration Rights Agreement”), pursuant to which, among other things, the Company agreed to register for resale on Form S-1 or, if available, Form S-3, pursuant to Rule 415 under the Securities Act, certain securities of the Company that are held by Sponsor.

Under the A&R Registration Rights Agreement, the Company agreed to indemnify holders of registrable securities and their respective officers, directors and each person who controls such holders (within the meaning of the Securities Act) against all losses, claims, damages, liabilities and expenses (including attorneys’ fees) resulting from any untrue or alleged untrue statement, or omission or alleged omission of a material fact in any registration statement, prospectus or any amendment thereof or supplement thereto pursuant to which such holders sell their registrable securities, unless such liability arose from such holder’s misstatement or alleged misstatement, or omission or alleged omission, and such holders agreed to indemnify the Company, its officers and directors and agents and each person who controls the Company (within the meaning of the Securities Act) against any losses, claims, damages, liabilities and expenses (including without limitation reasonable attorneys’ fees) resulting from any untrue statement of material facts or any omission of a material fact in any registration statement, prospectus or any amendment thereof or supplement thereto pursuant to which such holders sell their registrable securities.

Company Registration Rights Agreement

In connection with the closing of the Acquisition Merger, the Company, Dothan Independent and certain members of CPH (the “Company Members”) entered into a Registration Rights Agreement (the “Company Registration Rights Agreement”), pursuant to which certain members of CPH were granted customary registration rights with respect to the Company securities held by such parties following the Closing of the Business Combination. In certain circumstances, the Company Members can demand the Company’s assistance with underwritten offerings and block trades, and the Company Members are entitled to certain piggyback registration rights.

Under the Company Registration Rights Agreement, the Company agreed to indemnify the Company Members and their respective officers, directors and each person who controls such holders (within the meaning of the Securities Act) against all losses, claims, damages, liabilities and expenses (including attorneys’ fees) resulting from any untrue or alleged untrue statement, or omission or alleged omission of a material fact in any registration statement, prospectus or any amendment thereof or supplement thereto pursuant to which such holders sell their registrable securities, unless such liability arose from such holder’s misstatement or alleged misstatement, or omission or alleged omission, and such holders agreed to indemnify the Company, its officers and directors and agents and each person who controls the Company (within the meaning of the Securities Act) against any losses, claims, damages, liabilities and expenses (including without limitation reasonable attorneys’ fees) resulting from any untrue statement of material facts or any omission of a material fact in any registration statement, prospectus or any amendment thereof or supplement thereto pursuant to which such holders sell their registrable securities.

Indemnification of Directors and Officers

Concurrently with the Closing, the Company entered into indemnification agreements with its directors and executive officers. Each indemnification agreement provides that, subject to limited exceptions, the Company will indemnify the applicable indemnified person to the fullest extent permitted by law for claims arising in his or her capacity as a director or officer of the Company, as applicable.

11

Table of Contents

Forward Purchase Agreement

On April 6, 2026, Haymaker and the Company entered into a forward purchase agreement (the “Forward Purchase Agreement”) with each of Harraden Circle Investors, LP (“HCI”), Harraden Circle Special Opportunities, LP (“HCSO”), Harraden Circle Strategic Investments, LP (“HCSI”) and Harraden Circle Concentrated, LP (“HCC”) (with HCI, HCSO, HCSI, HCC, collectively as “Seller” or “Harraden”) for a prepaid share forward transaction. Pursuant to the terms of the Forward Purchase Agreement, the Seller agreed to purchase up to 5,000,000 Shares (as defined in the Forward Purchase Agreement) in accordance with the terms and conditions therein. Pursuant to the Forward Purchase Agreement, the Seller was prepaid an aggregate cash amount (the “Prepayment Amount”) equal to the (i) number of Shares, multiplied by (ii) the per-share redemption price at the closing of the Business Combination (the “Initial Price”), directly from Haymaker’s trust account in connection with the closing of the Business Combination. From time to time and on any business day on which Nasdaq and commercial banks in the City of New York are open for business (an “Exchange Business Day”), following the closing of the Business Combination (any such date, an “OET Date”), and subject to the terms and conditions therein, the Seller is required to terminate the transaction in whole or in part with respect to any number of Shares that are sold by Seller on such OET Date by giving notice of such termination and the specified number of Shares (such quantity, the “Terminated Shares”). As of each OET Date, the Company will be entitled to receive from Seller, and Seller shall pay to the Company, an amount equal to (a) the Initial Price multiplied by (b) the Terminated Shares. The Forward Purchase Agreement maturity date will be the earlier of (a) six months after the closing of the Business Combination, or (b) 10 Exchange Business Days following the date upon which the Company, in its sole discretion, delivers written notice to Seller that the Company is accelerating the maturity date; provided that such notice will not be effective until three months after the closing of the Business Combination. In addition, the Company has the right, in its sole discretion, to extend the maturity up to two times by three months each time by delivering written notice to Seller at least 10 Exchange Business Days in advance of the then-scheduled maturity date. At maturity, in exchange for the return of the number of remaining Shares under the Forward Purchase Agreement, the Seller shall retain an amount equal to (i) the number of Shares multiplied by (ii) the Initial Price. The Seller also agreed to waive any redemption rights with respect to the Shares during the term of the Forward Purchase Agreement. As of May 6, 2026, the Seller has sold 2.32 million shares of Class A Common Stock and has paid to the Company an aggregate of approximately $26.9 million, pursuant to the terms of the Forward Purchase Agreement.

Credit Agreement Amendments

Certain of the Company’s subsidiaries are party to a credit agreement (the “Credit Agreement”) with Bank of America, N.A., as administrative agent and certain lenders party thereto (the “Lenders”) providing for a fully drawn senior secured first lien term loan facility in the aggregate principal amount of $205 million (the “Term Loan”) and a $25 million revolving credit facility (the “Revolving Credit Facility”). On March 25, 2026, certain of the Company’s subsidiaries entered into that certain Consent and Second Amendment to Credit Agreement and First Amendment to Security and Pledge Agreement (the “Second Amendment”) to, among other things, permit the consummation of the Business Combination and giving effect to the Closing, to add the Company and SPAC as guarantors under the Credit Agreement. On April 7, 2026, certain of the Company’s subsidiaries and, giving effect to the Closing, the Company and SPAC, entered into that certain Limited Consent and Third Amendment to Credit Agreement (the “Third Amendment”) to, among other things, permit the Forward Purchase Agreement. On April 28, 2026, the Company and certain of the Company’s subsidiaries entered into that certain Limited Consent and Fourth Amendment to Credit Agreement (the “Fourth Amendment,” and the Credit Agreement, as amended through the date of the Fourth Amendment, the “Amended Credit Agreement”) to, among other things, permit the consummation of certain acquisitions, including the joinder to the Amended Credit Agreement of Purchaser Holdco, which was formed in connection with the Hope Acquisition.

12

Table of Contents

Dothan Management Agreement Amendment

Pursuant to the Business Combination Agreement, on the Closing Date, the Company entered into an amendment (the “Dothan Management Agreement Amendment”) to that certain Management and Consulting Agreement, dated as of July 29, 2024, by and between Dothan Concrete Investments Management, LLC (“Dothan Management”) and CPH (the “Dothan Management Agreement”). Among other things, the Dothan Management Agreement Amendment provides for (i) the assumption of the Dothan Management Agreement by the Company from CPH, (ii) payment by the Company to Dothan Management of diligence and integration fees in the amount of $10 million as the diligence and integration fee in consideration for the services provided by Dothan Management and its personnel to the Company in relation to the Business Combination, and (iii) quarterly consulting payments by the Company to Dothan Management. Dothan Management is an affiliate of the Company, Dothan Independent and SunTx Capital Management Corp. (“SunTx Capital Management”).

Corporate Information

Suncrete’s principal executive offices are located at 521 E. 2nd Street, Tulsa, Oklahoma 74120, and its telephone number is (918) 355-5700. Suncrete’s website is www.suncrete.com. Information found on or accessible through our website is not incorporated by reference into this prospectus and should not be considered part of this prospectus.

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). For so long as we remain an emerging growth company, we are permitted, and currently intend, to rely on the following provisions of the JOBS Act that contain exceptions from disclosure and other requirements that otherwise are applicable to public companies and file periodic reports with the SEC. These provisions include, but are not limited to:

| • | being permitted to present only two years of audited financial statements and selected financial data and only two years of related “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our periodic reports and registration statements, including this prospectus, subject to certain exceptions; |

| • | not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley”), as amended; |

| • | reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements, and registration statements, including in this prospectus; |

| • | not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements; and |

| • | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

We will remain an emerging growth company until the earliest to occur of:

| • | the fifth anniversary of the date of our first sale of common equity securities pursuant to an effective registration statement; |

| • | the last day of the fiscal year, in which we have total annual gross revenue of at least $1.235 billion, adjusted yearly for inflation; |

| • | the date on which we are deemed to be a “large accelerated filer,” as defined in the Exchange Act; and |

| • | the date on which we have issued more than $1 billion in non-convertible debt over a three-year period. |

13

Table of Contents

We have elected to take advantage of certain of the reduced disclosure obligations in this prospectus and may elect to take advantage of other reduced reporting requirements in our future filings with the SEC. As a result, the information that we provide to holders of our stockholders may be different than what you might receive from other public reporting companies in which you hold equity interests.

We have elected to avail ourselves of the provision of the JOBS Act that permits emerging growth companies to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. As a result, we will not be subject to new or revised accounting standards at the same time as other public companies that are not emerging growth companies.

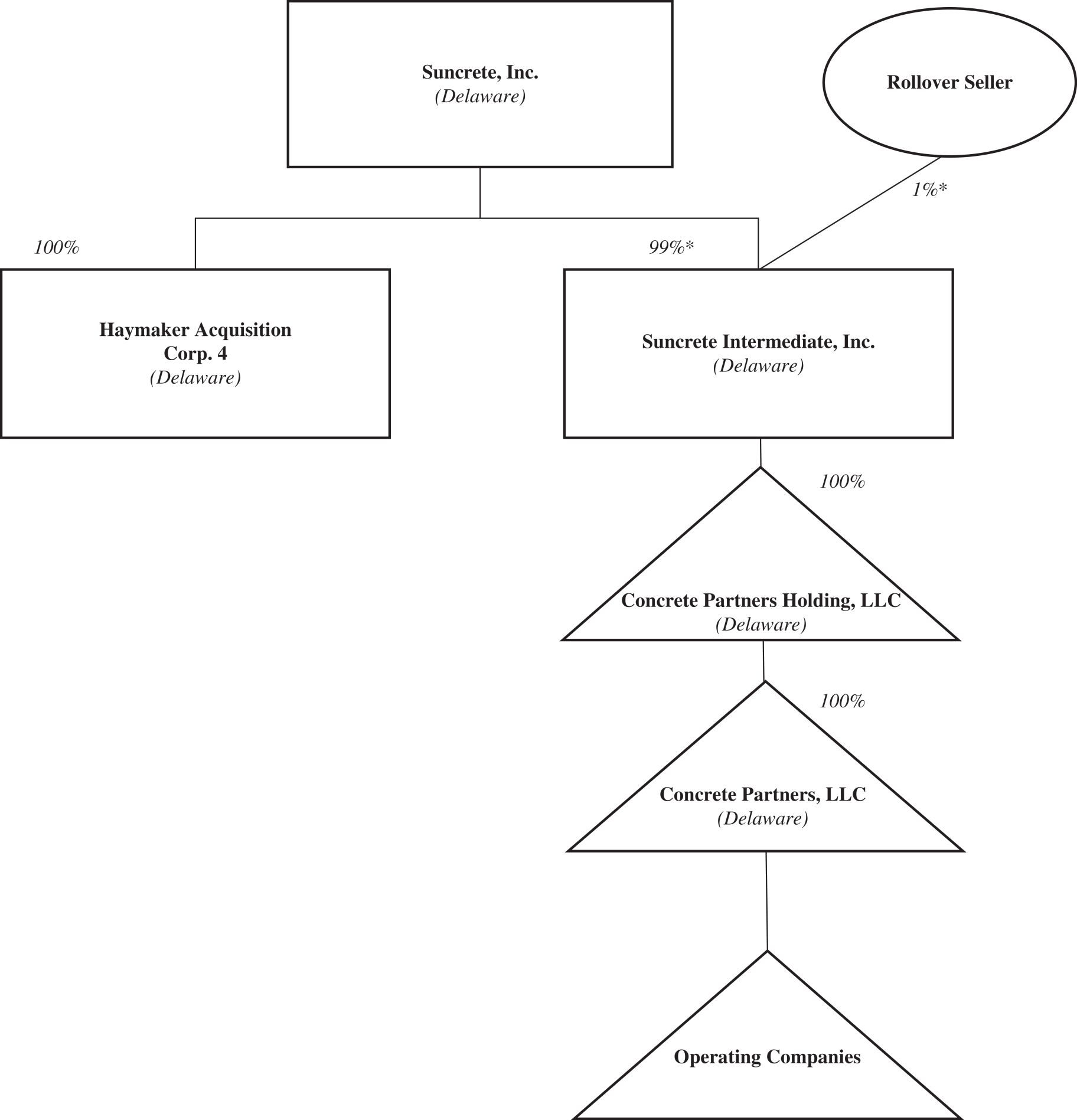

Organizational Structure

Current Structure

The following simplified diagram, which excludes multiple legal entities, illustrates our organizational structure as of May 7, 2026, following the Business Combination and the other acquisitions described under “Recent Developments” above.

14

Table of Contents

| * | Suncrete, Inc. holds all of the 7,403,459 issued and outstanding shares of Class A common stock, par value $0.0001 per share (the “Holdco Class A Common Shares”), of Suncrete Intermediate, Inc., and the issued and outstanding 69,511 HoldCo Class B Common Shares are held by the one of the Sellers in the Hope Acquisition. The HoldCo Class B Shares are nonvoting and have no dividend or liquidation rights. The HoldCo Class B Shares are exchangeable on a 10-to-1 basis for an aggregate of 695,110 shares of Class A Common Stock of the Company on the terms and subject to the conditions set forth in the Hope Exchange Agreement. |

Summary of Risk Factors

The risk factors summarized below could materially harm our business, operating results and/or financial condition, impair our future prospects and/or cause the price of our ordinary shares to decline. These risks are

15

Table of Contents

discussed more fully following this summary. Material risks that may affect our business, operating results and financial condition include, but are not necessarily limited to, the following:

| • | There are risks related to our operating strategy. |

| • | Our failure to successfully identify, complete, manage and integrate acquisitions could reduce our earnings and slow our growth. |

| • | A significant slowdown or decline in economic conditions, particularly in the southern United States, could adversely impact our results of operations. |

| • | Because our industry is capital-intensive and we have significant fixed and semi-fixed costs, our profitability is sensitive to changes in volume. |

| • | Reduced demand for new home construction could adversely affect the residential construction market, which could affect our financial position, operating results and liquidity. |

| • | Our operating results may vary significantly from one reporting period to another and may be adversely affected by the cyclical nature of the markets we serve. |

| • | A significant downturn in the construction industry may result in an impairment of our goodwill. |

| • | Our business is seasonal and subject to adverse weather. |

| • | Our business depends on the availability of sand and aggregate reserves or deposits and our ability to obtain or mine them economically. |

| • | We may lose business to competitors who underbid us, and we may be otherwise unable to compete favorably in our highly competitive industry. |

| • | We depend on our information technology systems and processes, which are subject to cybersecurity and data leakage risks. |

| • | We depend on third parties for concrete equipment and materials essential to operate our business. |

| • | We use large amounts of electricity and diesel fuel that are subject to potential reliability issues, supply constraints, and significant price fluctuation, which could affect our financial position, operating results and liquidity. |

| • | Delays or interruptions of our transportation logistics could affect operating results. |

| • | Our results of operations can be adversely affected by labor shortages, turnover and labor cost increases. |

| • | Our business depends on federal, state and local government spending for public infrastructure construction, and reductions in government funding could adversely affect our results of operations. |

| • | Governmental regulations, including environmental regulations, may result in increases in our operating costs and capital expenditures and decreases in our earnings. |

| • | Our operations are subject to various hazards, including natural disasters, that may cause personal injury or property damage for which we have a limited amount of insurance, and our business, operating costs and profitability could be adversely affected. |

| • | Our substantial indebtedness could adversely affect our financial condition and prevent us from fulfilling our obligations. |

| • | The Credit Agreement restricts our ability to engage in some business and financial transactions. |

| • | We may need to raise additional capital in the future, and we may not be able to do so on favorable terms or at all, which could impair our ability to operate our business or achieve our growth objectives. |

16

Table of Contents

| • | There can be no assurance that the shares of our Class A Common Stock will be able to comply with the continued listing rules of Nasdaq. |

| • | The price of our Class A Common Stock may change significantly and you could lose all or part of your investment as a result. |

| • | The dual class structure of our Common Stock has the effect of concentrating voting control with holders of our Class B Common Stock, which limits the ability of holders of our Class A Common Stock to influence corporate matters. |

| • | Future sales, or the perception of future sales, of our Class A Common Stock by us or our stockholders in the public market could cause the market price for our Class A Common Stock to decline. |

| • | The SunTx Group controls the Company, and their interests may conflict with the interests of the Company or yours in the future. |

| • | We are currently an emerging growth company within the meaning of the Securities Act, and to the extent we have taken advantage of certain exemptions from disclosure requirements available to emerging growth companies, this could make our securities less attractive to investors and may make it more difficult to compare our performance with other public companies. |

| • | Provisions in our Organizational Documents and Delaware corporate law make it more difficult to effect a change in control, which could adversely affect the price of our Class A Common Stock. |

| • | The Certificate of Incorporation designates certain courts as the sole and exclusive forum for certain types of actions and proceedings that may be initiated by our stockholders, which could limit the ability of our stockholders to obtain a favorable judicial forum for disputes with us or our directors, officers or other employees. |

| • | We are a “controlled company” under Nasdaq listing rules. As a result, our stockholders do not have, and may never have, certain corporate governance protections that are available to stockholders of companies that are not controlled companies. |

| • | A substantial number of shares of our securities are restricted securities and, as a result, there may be limited liquidity for our Class A Common Stock. |

| • | Certain existing securityholders acquired their securities in the Company at prices below the current trading price of such securities, and may experience a positive rate of return based on the current trading price. Future investors in our Company may not experience a similar rate of return. |

17

Table of Contents

RISK FACTORS

Any investment in our securities involves a high degree of risk. You should carefully consider all of the information contained in this prospectus and any subsequent prospectus supplement, including our financial statements and related notes thereto, before investing in our securities. However, such risks and those discussed elsewhere in any subsequent prospectus supplement are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect us. If any of the risks described in any subsequent prospectus supplement or others not specified therein materialize, our business, financial condition and results of operations could be materially and adversely affected. In that case, you may lose all or part of your investment.

Unless the context otherwise requires, all references in this subsection to the “Company,” “Suncrete,” “we,” “us,” or “our” refer to the business of Suncrete and its consolidated subsidiaries.

Risks Related to Our Operations

There are risks related to our operating strategy.

A key component of our operating strategy is to operate our businesses on a decentralized basis, with local or regional management retaining responsibility for day-to-day operations, profitability and the internal growth of the individual business. If we do not implement and maintain proper overall business controls, this decentralized operating strategy could result in inconsistent operating and financial practices and our overall profitability could be adversely affected.

Our failure to successfully identify, complete, manage and integrate acquisitions could reduce our earnings and slow our growth.

We (including our predecessors) have acquired nine companies since 2016, including the recent Thunder Acquisition, Hope Acquisition and Nelson Acquisition. As part of our strategy to pursue growth opportunities in the Sunbelt region of the United States, we will continue to evaluate strategic acquisition opportunities that we believe have the potential to support and strengthen our business. We cannot predict the timing or size of any future acquisitions. Intense competition exists for acquisition opportunities in our industry. Competition for acquisitions may increase the cost of, or cause us to refrain from, completing acquisitions. We may be unable to identify and complete acquisitions on favorable terms, or at all. Our ability to complete acquisitions is dependent upon, among other things, the willingness of acquisition candidates we identify to sell, our ability to obtain financing or capital, if needed, on satisfactory terms, and, in some cases, regulatory approvals. The investigation of acquisition candidates and the negotiation, drafting and execution of relevant agreements requires substantial management time and attention and substantial costs for accountants, attorneys and others. If we fail to complete any acquisition for any reason, including events beyond our control, the costs incurred up to that point for the proposed acquisition likely would not be recoverable.

Acquisitions typically require integration of the acquired company’s estimation, project management, finance, information technology, risk management, purchasing and fleet management functions. We may be unable to successfully integrate businesses we acquire, including the businesses of the Schwarz Entities, Hope and Nelson Bros. into our existing business, and acquired businesses may not be as profitable as we had expected or at all. Acquisitions involve risks that the acquired business will not perform as expected and that our expectations concerning the value, strengths and weaknesses of the acquired business will prove incorrect.

We have expanded into the Texas and Louisiana markets in connection with the recent Hope Acquisition and Nelson Acquisition, and future acquisition targets may be in geographic regions in which we do not currently operate, which could result in unforeseen operating difficulties and difficulties in coordinating geographically dispersed operations, personnel and facilities. In addition, as we enter into new geographic markets, we have

18

Table of Contents

become subject to, and may in the future become subject to, additional and unfamiliar legal and regulatory requirements. Compliance with regulatory requirements may impose substantial additional obligations on us and our management, cause us to expend additional time and resources in compliance activities and increase our exposure to penalties or fines for non-compliance with such additional legal requirements. Our recently completed acquisitions and any future acquisitions could cause us to become involved in labor, commercial, or regulatory disputes or litigation related to any new enterprises and could require us to invest further in operational, financial and management information systems and to attract, retain, motivate and effectively manage local or regional management and additional employees. Upon completion of an acquisition, key members of the acquired company management team may resign, which could require us to attract and retain new management and could make it difficult to maintain customer relationships. Our inability to effectively manage the integration of our completed and future acquisitions could prevent us from realizing expected rates of return on an acquired business and could have a material and adverse effect on our business, financial condition, results of operations, liquidity and cash flows.

We cannot guarantee that we will achieve synergies and cost savings in connection with recent and future acquisitions. Businesses that we may acquire could have unaudited financial statements that were prepared by management and were not independently reviewed or audited, and such financial statements could be materially different if they were independently reviewed or audited. We cannot guarantee that we will continue to acquire businesses at valuations consistent with our prior acquisitions or that we will complete future acquisitions at all. In addition, our results of operations from these acquisitions could, in the future, result in impairment charges for any of our intangible assets, including goodwill or other long-lived assets, particularly if economic conditions worsen unexpectedly.

A significant slowdown or decline in economic conditions, particularly in the southern United States, could adversely impact our results of operations.

We currently sell our ready-mix concrete and sand products to the construction industry in Arkansas, Oklahoma, Texas and Louisiana. A significant slowdown or decline in economic conditions or uncertainty regarding the economic outlook in the United States generally, or in the states in which we operate particularly, could reduce demand in the construction industry in our markets. Construction spending is also affected by changes in interest rates, demographic shifts, industry cycles, employment levels, inflation and other business, economic and financial factors, any of which could contribute to a downturn in construction activities or spending in these states. In addition, any instability in the financial and credit markets could negatively impact our customers’ ability to pay us on a timely basis, or at all, for work on projects already in progress, could cause our customers to delay or cancel projects in our contract backlog and could create difficulties for customers to obtain adequate financing to fund new projects, including through the issuance of municipal bonds.

Because our industry is capital-intensive and we have significant fixed and semi-fixed costs, our profitability is sensitive to changes in volume.

The property, plants and equipment needed to produce our products and provide our services are expensive. We must spend a substantial amount of capital to purchase and maintain such assets. Although we believe our current cash balance, along with our projected internal cash flows and available financing sources, will provide sufficient cash to support our currently anticipated operating and capital needs, if we are unable to generate sufficient cash to purchase and maintain the property, plants and equipment necessary to operate our business, or if the timing of payments on our receivables is delayed, we may be required to reduce or delay planned capital expenditures or to incur indebtedness. In addition, due to the level of fixed and semi-fixed costs associated with our business, volume decreases could have a material adverse effect on our financial condition, results of operations or liquidity.

19

Table of Contents

Reduced demand for new home construction could adversely affect the residential construction market, which could affect our financial position, operating results and liquidity.

Approximately 36.7% of our revenue for the fiscal year ended December 31, 2025, was from residential construction contractors. Tightening of mortgage lending, mortgage financing requirements or higher interest rates could adversely affect the ability to obtain credit for some borrowers, or reduce the demand for new home construction, which could have a material adverse effect on our business and results of operations. In addition, the limitation of the home mortgage interest and property tax deductions could reduce the demand for new home construction, which could have a material adverse effect on our business and results of operations. Additionally, a decrease in current migration inflow patterns or increased population outflow could reduce the demand for new home construction in the areas in which we operate. A downturn in new home construction could also adversely affect our customers focused on residential construction, possibly resulting in slower payments, higher default rates in our accounts receivable and an overall increase in working capital.

Our operating results may vary significantly from one reporting period to another and may be adversely affected by the cyclical nature of the markets we serve.

The relative demand for our products is a function of the highly cyclical construction industry. As a result, our revenue may be adversely affected by declines in the construction industry generally and in our local markets. Our results also may be materially affected by:

| • | the level of commercial and residential construction in our local markets, including reductions in the demand for new residential housing construction below current or historical levels; |

| • | the availability of funds for public or infrastructure construction from local, state and federal sources; |

| • | unexpected events that delay or adversely affect our ability to deliver concrete according to our customers’ requirements; |

| • | changes in interest rates and lending standards; |

| • | changes in the mix of our customers and business, which result in periodic variations in the margins on jobs performed during any particular quarter; |

| • | the timing and cost of acquisitions and difficulties or costs encountered when integrating acquisitions; |

| • | the budgetary spending patterns of customers; |

| • | increases in construction and design costs; |

| • | power outages and other unexpected delays; |

| • | our ability to control costs and maintain quality; |

| • | pricing pressure due to changes in asset utilization or economic weakness; |

| • | employment levels; and |

| • | regional or general economic conditions. |

Accordingly, our operating results in any particular quarter may not be indicative of the results that you can expect for any other quarter or for the entire year. Furthermore, negative trends in the ready-mix concrete or aggregates industries or in our geographic markets could have material adverse effects on our business, financial condition, results of operations, liquidity and cash flows.

A significant downturn in the construction industry may result in an impairment of our goodwill.

We test goodwill for impairment if events or circumstances change in a manner that would more likely than not reduce the fair value of a reporting unit below its carrying value. During such impairment testing, we may

20

Table of Contents

identify events or changes in circumstances that could indicate the fair value of one or more of our reporting units is below its carrying value. For example, a significant downturn in the construction industry may have an adverse effect on the fair value of our reporting units. A decrease in the estimated fair value of one or more of our reporting units could result in the recognition of a material, non-cash write-down of goodwill.

Our business is seasonal and subject to adverse weather.

Because our business is primarily conducted outdoors, erratic weather patterns, seasonal changes and other weather-related conditions affect our business. Adverse weather conditions, including tornados, cold weather, snow and heavy or sustained rainfall, reduce construction activity, restrict the demand for our products and impede our ability to efficiently deliver concrete. For example, our operating results during 2025 were significantly impacted by unusually heavy and sustained rainfall across Oklahoma and Arkansas during the year, which limited construction activity and reduced delivery days. Adverse weather conditions could also increase our costs and reduce our production output as a result of power loss, needed plant and equipment repairs, delays in obtaining permits, time required to remove water from flooded operations and similar events. In addition, during periods of extended adverse weather or other operational delays, we may elect to continue to pay certain hourly employees to maintain our workforce, which may adversely impact our results of operations. Severe drought conditions can also restrict available water supplies and restrict production. Consequently, these events could adversely affect our business, financial condition, results of operations, liquidity and cash flows.

Our business depends on the availability of sand and aggregate reserves or deposits and our ability to obtain or mine them economically.